Homeowners’ associations (HOA) are designed to manage common or shared property, protect owners’ property values, provide services to residents, and develop a sense of community through social activities and amenities.

People who belong to an HOA pay annual or monthly dues which the HOA uses to maintain shared spaces (common areas) and carry out other association duties like rule enforcement, records management, and financial planning. Homeowners agree to follow the rules and pay the HOA fees in exchange for a harmonious place to live, access to the amenities and some assurance that their property values will be professionally maintained.

An elected board of volunteers runs the HOA on behalf of all community homeowners. The HOA board typically works together with a management company to ensure the responsibilities of the association are carried out according to their rules, regulations, governing documents, and all applicable local, state, and federal laws.

In California, HOAs are organized as mutual-benefit nonprofit corporations and are subjected to all laws that regulate matters of corporate governance. Further, HOAs are governed by the Davis-Stirling Act (California Civil Code sections 4000, et. seq) and various sections of other California laws and regulations.

An HOA’s authority is obtained from its declarations (CC&R), a document that is recorded with the county clerk’s office when the community is formed. The CC&R legally establishes the association and proclaims the association is organized under California law. The HOA’s covenants (agreement between owners and association), restrictions (forbidden actions or limitations of real estate and common areas in the community), and conditions/powers/duties of the board of directors will be all outlined in the association’s CC&R and Bylaws.

Our HOA consists of a board of five directors (president, vice-president, treasurer, secretary and director). They each serve 2-year, staggered terms. Every year, the HOA members (homeowners) elect two (odd-numbered years) or three (even-numbered years) directors.

Powers and duties entrusted to the board include authorization to collect homeowner assessments, arrange maintenance services for common areas or amenities, enforce the association’s covenants, and act on the behalf of the association in any legal, contractual, or financial matters.

Our Bylaws establish the regulations and procedures for HOA elections, board member/officer appointments, a board of directors or member meetings, and the requirements to amend the community’s governing documents.

Our Bylaws and CC&R generally allow the board of directors to adopt and implement what are known as Rules and Regulations to further define the community’s policies and intentions. The Rules and Regulations document can be found in the Governing Documents section of this website.

The board is assisted in its task by a set of committees made up of volunteer members of the association and by a professional management staff.

The committees research alternatives and present recommendations to the board. There is a great deal of behind-the-scenes work performed before any proposal reaches the board for a vote.

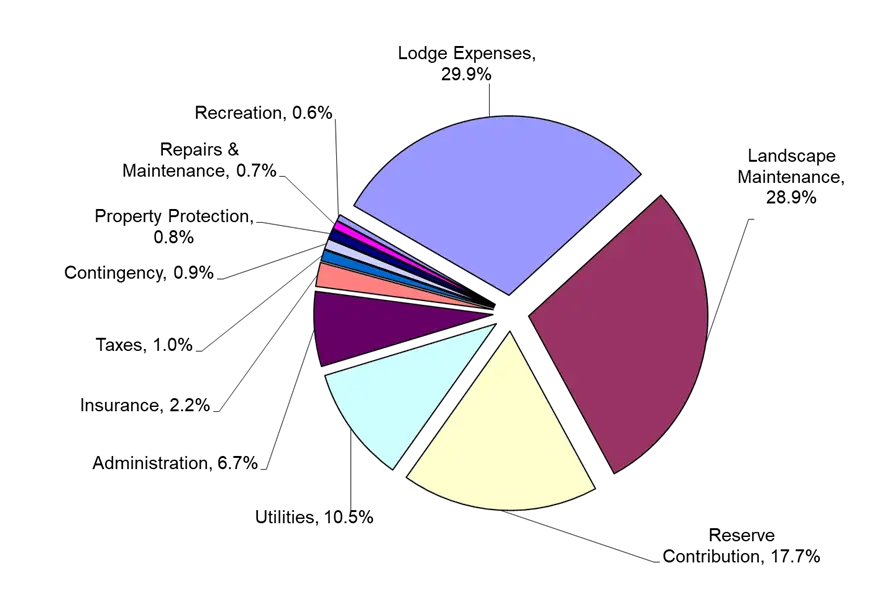

Providing maintenance of the common areas, protecting owners’ property values, providing services to residents, and developing a sense of community through social activities and amenities comes at a cost. That cost is set forth in monthly assessments charged to each property owner.

Four Seasons at Bakersfield has many amenities and provides additional services that other active-adult communities in town do not. Thus, our monthly assessments are slightly higher than those of other communities. For instance, the HOA provides front yard landscaping – mowing grass, trimming trees, planting flowers, irrigation, etc. Landscaping costs, including the common areas are about 1/3 of the monthly HOA fee.

A slightly larger 1/3 of the HOA fee pays for our professional management services which includes full time, on-site staff. The management staff assist the board by enforcing the rules, arranging activities, collecting dues, managing our records, overseeing maintenance of the amenities and grounds and providing office services.

Another 18% goes to setting aside money for maintenance in a reserve fund. Since we have more amenities than most HOA’s this cost will be higher than theirs.

The HOA Fees for 2026 is $445.00 per month.

HOA homeowners should expect HOA fees to increase each year approximately equal to the rise in the cost of living. The cost of living or Consumer Price Index (CPI) is calculated by the government as a measure of the buying power of the dollar.

The Board of Directors and all of the committees are constantly looking for ways to reduce our costs without risking a restriction in services or amenities or reduction in home value due to inadequate maintenance. But in spite of their best efforts, the board cannot perform their duty to maintain home values without a budget that sets the HOA fees that match actual costs.

In 2010 that was $250. But due to inflation, that same buying power is $382 in 2025 dollars. So, when inflation is considered, our HOA fees are now only 7.6% higher than they were in 2010.

From 2010 until 2015 the HOA Fee was held at $250 since it was subsidized by the builder, K. Hovnanian. From 2016 to 2019, after the builder left, the board chose to hold the HOA fees low by spending down the reserve fund rather than raise the fees to cover costs. But that was unsustainable. So, starting in 2020 the board gradually increased the HOA fees until they matched the actual costs. Since 2023, the HOA fees are ahead of the CPI enabling us to replenish our reserve fund.

Under the law, an HOA cannot borrow money. So rather than making monthly payments to pay back loans, they must set aside just enough money each month (in the reserve fund) so that when large maintenance costs do occur there is just enough money to pay the bill.

To figure out how much money to set aside each month, the board pays professionals (currently California Builder Services) to physically inspect our assets every three years, and review yearly, to determine just how much will be needed and when it will be needed in the reserve fund based on the expected life of each asset.

If the professionals predict accurately, and the board choses to contribute to the reserve fund at that level, there is little chance that the reserve fund will run out of money. But if it does, the HOA will have to ask the homeowners for an additional payment to cover the shortfall.

At the end-of -the -year 2025 the Reserve Fund will be 51%. The amount of the contribution to the fund each month is now such that the reserves will gradually grow and return to a healthier level.